The structure.

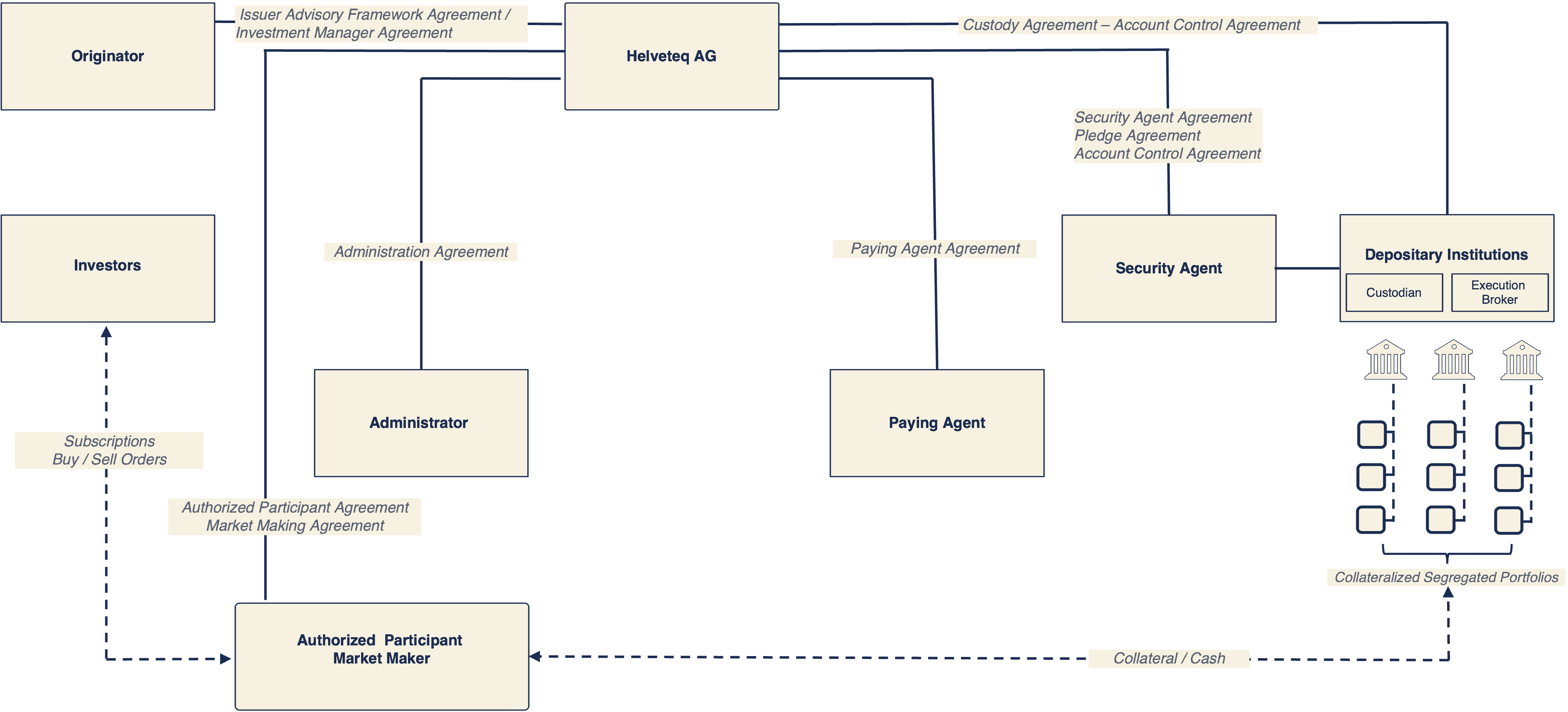

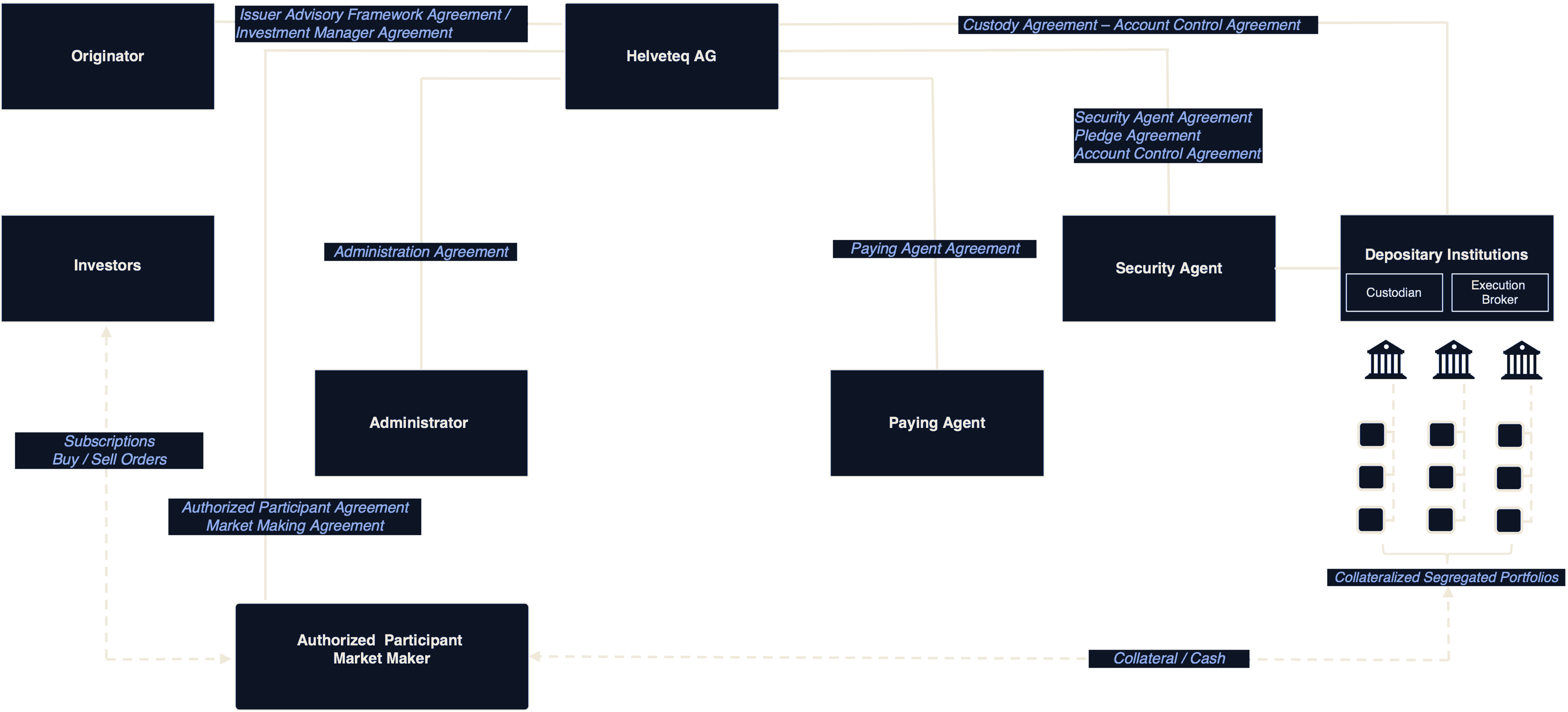

The diagram shows the full structure of a Helveteq issuance. Helveteq AG is the Issuer. The Originator contributes the underlying. The Investor subscribes through their bank. The Custodian holds the Collateral. The Security Agent holds the Pledge for the benefit of investors. The Paying Agent operates the cash and securities legs through SIX SIS. Every solid line is a signed bilateral agreement. Every dashed line is an operational flow.

How a product is created.

KYI

Helveteq performs Know-Your-Intermediary due diligence on the Originator and, where applicable, the Asset Manager.

IAFA

The Issuance Advisory Framework Agreement is the commercial mandate between Helveteq and the client. It defines scope, fees and term.

Structuring

Every Helveteq product is a Tracker Certificate under SSPA category 1300. The product is commercialised as ETP, nETP or AMC depending on three independent variables:

- Listing. Listed (ETP) or non-listed (nETP). Depends on the eligibility of the underlying under the SIX listing rules and the availability of a market maker.

- Retail eligibility. Retail-eligible or restricted to professional investors. Depends on the underlying, the availability of a Key Information Document (KID), and the applicable liquidity rules.

- Strategy type. Passive, rule-based or discretionary. Where the strategy is discretionary, the Asset Manager is appointed under a separate agreement and must be FinIA-licensed.

The Custodian is selected per asset class. The Security Agent is appointed under a Pledge Agreement and an Account Control Agreement.

Final Terms

Each product is issued under Final Terms, which extend the Base Prospectus approved by SIX Exchange Regulation and must be read in conjunction with it. Final Terms define the ISIN, the Underlying, the Issue Price, the fees, the Redemption Notice Period, and every other lifecycle parameter specific to that issuance.

ISIN live

Once Final Terms are signed and the Collateral is in place, the Paying Agent creates the Securities against payment through SIX SIS (DvP), and the ISIN goes live. Typically a matter of days from signed terms, depending on the underlying.

After issuance, NAV is calculated at the frequency defined in the Final Terms. Subscriptions and redemptions settle through SIX SIS. The Issuer's accounts are audited annually under IFRS.

What protects the investor.

A Helveteq product is a bearer debt security. The investor's claim runs against the Collateral, not against the general estate of Helveteq AG.

Full collateralisation

Every product is fully collateralised. The Collateral is held in a dedicated account at the Custodian, separated per product. No cross-pledging between products.

The Pledge

The Collateral is pledged in favour of an independent Security Agent for the benefit of investors, with the pledge perfected through an Account Control Agreement under Swiss law. In an issuer default, the Security Agent may enforce the collateral in accordance with the transaction documents. Collateralisation mitigates issuer credit risk but does not eliminate it.

The regulatory perimeter.

Helveteq AG is not FINMA-supervised. The Issuer sits outside the FinIA perimeter.

Specific counterparties in the chain are regulated for their respective activities. The Paying Agent is a FINMA-regulated Swiss bank operating its own AMLA framework. The Custodian is a FINMA-regulated Swiss bank or a specialised custodian operating under the equivalent Swiss requirements for its asset class.

Helveteq products are securities under FinSA, not collective investment schemes under CISA. They are bookable through investors' own banks. Helveteq does not custody investor assets, does not execute trades, does not provide investment advice, and does not distribute or place securities.

NEXT STEPS